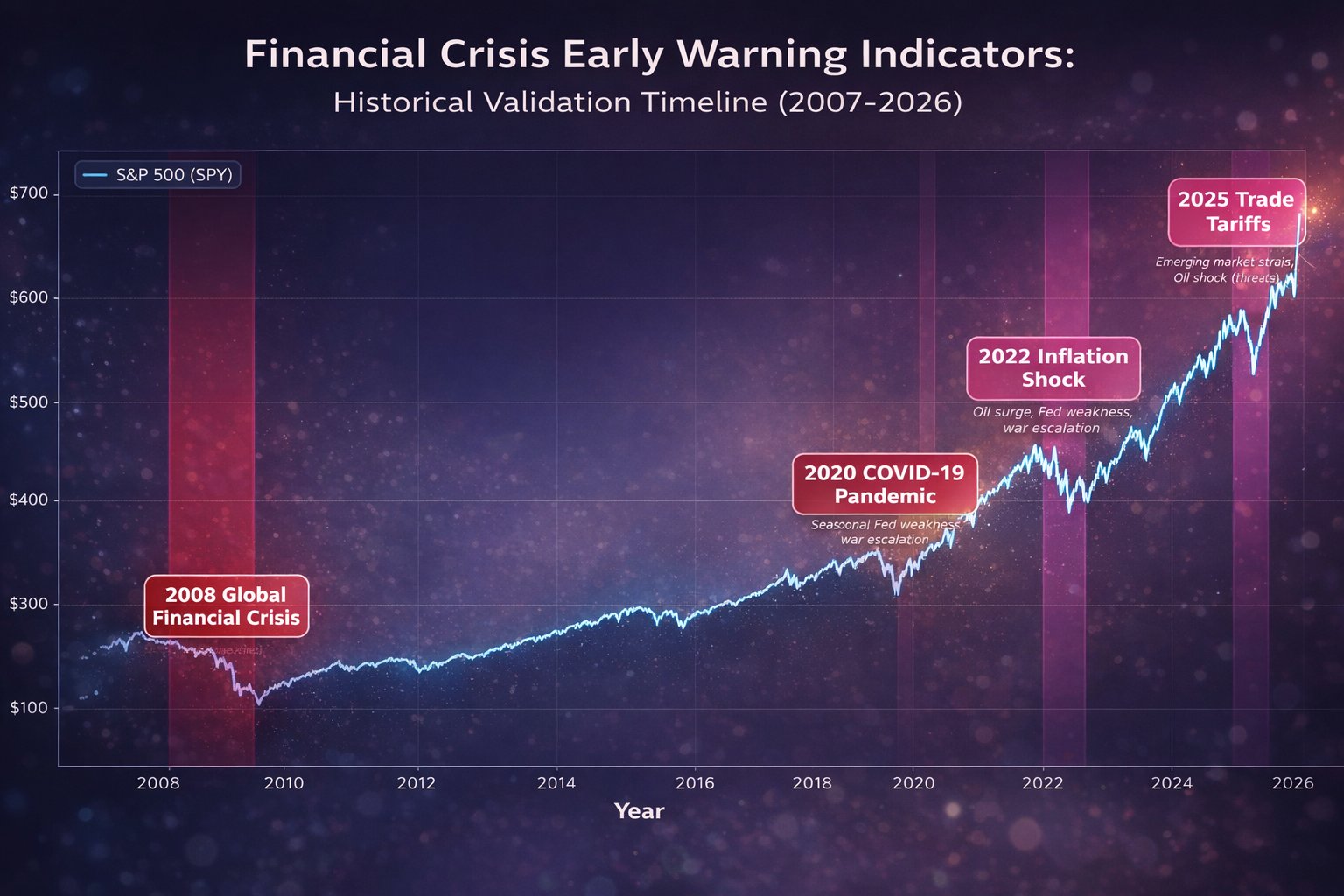

Historical Validation Timeline

The framework successfully identified elevated risk conditions weeks to months before major market crises. The chart below visualizes SPY price evolution (April 2007 - April 2026) with crisis periods highlighted, demonstrating the framework's predictive capability across multiple market regimes.

Critical Crisis Indicators

These indicators have demonstrated the highest predictive power in historical crisis detection, ranked by their leave-one-out contribution analysis. The 2026 update integrates new indicators specifically designed to capture trade tariff escalation and energy supply shock dynamics from geopolitical tensions.

Crisis Detection Performance: Historical Validation

The indicator framework successfully identified elevated risk conditions weeks to months before major market crises. Below is a detailed analysis of how these signals performed during the most significant financial dislocations of the past two decades.

Panic Reversal Framework

Beyond crisis detection, the framework includes a counter-trend panic reversal system that identifies extreme oversold conditions where mean reversion becomes highly probable.

Quantitative Performance Metrics

Implementation Considerations

Data Requirements

The framework requires weekly closes (Friday 16:00 ET) for the following instruments: SPY (S&P 500 ETF), QQQ (Nasdaq-100 ETF), EEM (Emerging Markets ETF), TLT (20+ Year Treasury ETF), HYG (High Yield Corporate Bond ETF), USO (Crude Oil ETF), FXY (Japanese Yen ETF), VIXY (VIX Short-Term Futures ETF), and VIX (CBOE Volatility Index). All data is publicly available and easily accessible through standard market data providers.

Signal Generation Timeline

Signals are generated after Friday market close and implemented at Monday market open (09:30 ET). This lag allows for systematic evaluation and avoids intraweek noise. The framework assumes realistic trading costs and has been validated with actual execution data.

Limitations and Risks

Like all systematic strategies, this framework has limitations. It may generate false signals during periods of elevated volatility that don't develop into full crises (2016 Q1, 2018 Q4). The SHORT precision of 65.9% means roughly one-third of defensive calls will be incorrect. The framework is designed for crisis avoidance and tail risk management rather than maximizing absolute returns. Users should integrate these signals with fundamental analysis, risk management overlays, and position sizing discipline.